You just picked up a speeding ticket months after an at-fault accident—and your carrier has already raised your rate once. Here's how New York carriers calculate the second surcharge and when the combined penalty finally drops.

How New York Carriers Calculate Two Separate Surcharges

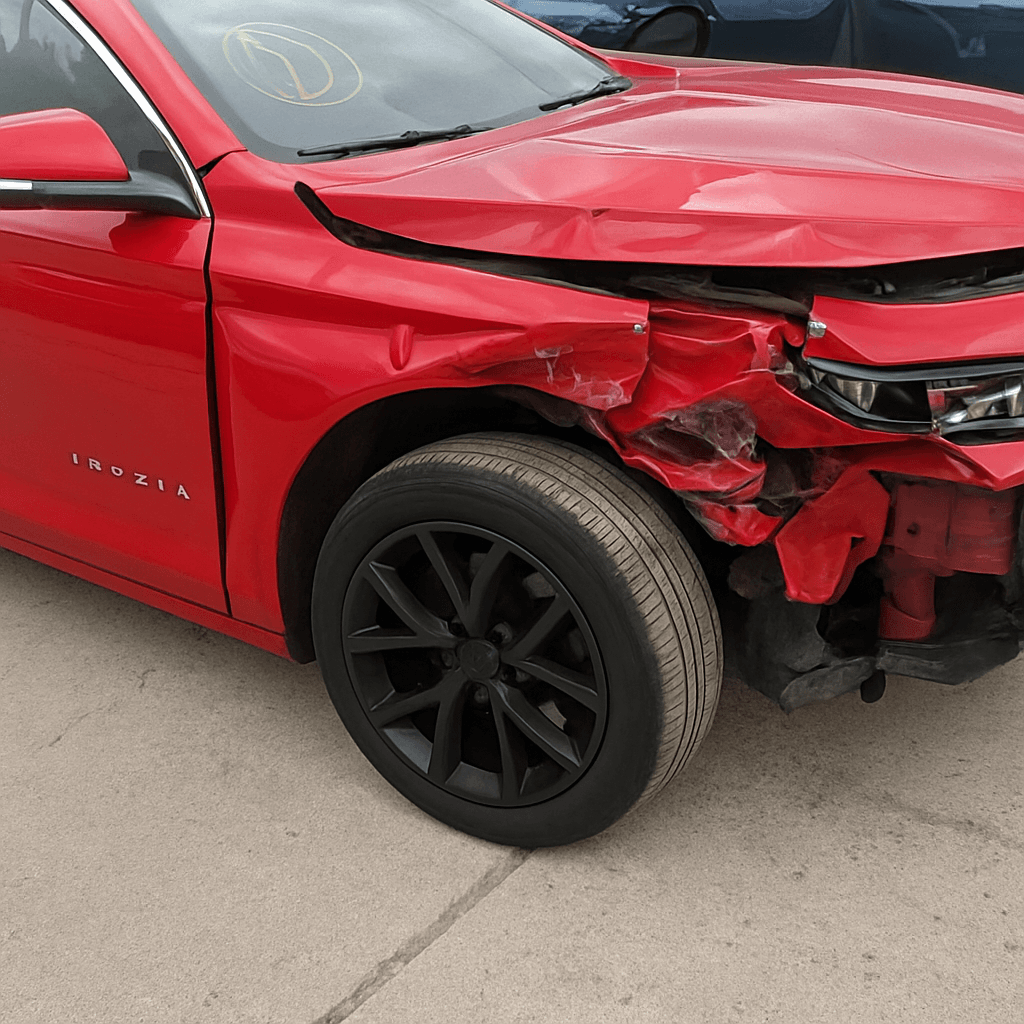

When you add a speeding ticket to a driving record that already carries an at-fault accident, most New York carriers apply two independent surcharges rather than combining them into a single penalty. The at-fault accident typically adds 20-40% to your premium from the claim closure date. The speeding ticket—even a minor 1-10 mph over conviction—adds another 15-25% calculated from the conviction date. A driver paying $150/mo before either event can expect $180-210/mo after the accident, then $207-262/mo once the ticket conviction posts.

Carriers treat accidents and moving violations as separate risk categories because they measure different behaviors. An at-fault accident reflects judgment or reaction time under specific road conditions. A speeding ticket reflects consistent speed choices across multiple driving sessions. Rating algorithms assign each event its own lookback window and surcharge curve, which is why the penalties stack rather than merge.

The combined surcharge creates immediate affordability pressure for drivers already stretched by the first increase. Many New York drivers discover the second penalty only at renewal, 30-90 days after the ticket conviction, when the carrier pulls an updated MVR. By that point, the prior accident surcharge has been in effect for months, and the household budget has already absorbed the first rate jump.

Why the Two Surcharges Expire on Different Schedules

Your at-fault accident surcharge typically remains active for 36-60 months from the claim closure date, depending on carrier and severity. The speeding ticket surcharge runs 36-48 months from the conviction date under current state DMV point rules. If your accident closed in January 2023 and your speeding ticket conviction posted in September 2023, the accident surcharge may expire in January 2026 while the ticket surcharge persists until September 2026—or longer if your carrier uses a 48-month lookback for moving violations.

New York assigns 3-11 points per speeding violation depending on excess speed, and those points remain on your DMV record for 18 months from conviction. Your insurance surcharge, however, follows the carrier's internal lookback window, not the DMV point expiration. A ticket that drops off your DMV abstract after 18 months will still affect your rate for another 18-30 months because carriers pull conviction dates from their own databases and apply their filed surcharge schedules independently.

Some carriers reduce the surcharge incrementally—dropping the penalty by 25-50% at the 24-month mark before eliminating it entirely at 36 months. Others maintain the full surcharge until the lookback window closes, then remove it in a single adjustment at renewal. You won't know which model your carrier uses unless you request a surcharge schedule explanation in writing or compare quotes from multiple carriers at the 24-month point.

Compare rates from carriers that work with drivers who have points

Standard carriers surcharge heavily after violations. These specialists price your specific record differently.

Get Your Free Quote✓ Violation Specialists✓ No Obligation✓ Licensed Carriers✓ All Point Levels

Which New York Carriers Write Two-Event Records and at What Price Tier

Most preferred carriers—State Farm, GEICO, Nationwide, Travelers—will keep you after one at-fault accident or one speeding ticket, but a second event within 36 months often triggers a declination notice at renewal or a non-renewal letter 60 days before your policy expires. Preferred carriers typically exit the account when combined surcharges push the driver into a loss ratio that exceeds their risk appetite, even if the driver remains below New York's 11-point suspension threshold.

Standard carriers like Progressive, Allstate, and Liberty Mutual often maintain coverage for drivers with two events, but they reclassify the policy into a higher-risk tier with correspondingly higher base rates. A driver paying $180/mo in a preferred tier before the second event may see $240-320/mo in a standard tier after both surcharges apply. The rate increase reflects both the surcharge percentages and the higher base rate in the new tier.

Non-standard carriers—Dairyland, The General, Safe Auto—specialize in multi-event records and will quote drivers with an accident plus a ticket, but monthly premiums in this market typically start at $280/mo and can exceed $400/mo depending on vehicle, coverage limits, and ZIP code. Non-standard policies often require six-month prepayment or monthly installment fees of $8-15, which further increases the effective monthly cost.

What Happens If You Add a Third Event Before the First Two Expire

A third moving violation or at-fault accident added before the first two events roll off your carrier's lookback window will likely trigger non-renewal from any standard or preferred carrier still covering you. New York uses an 11-point suspension threshold within 18 months, and three events in three years—even if no single event carries enough points to suspend your license—signals habitual risk that most carriers will not underwrite.

If the third event pushes you to or past 11 points, your license suspends and you enter a mandatory revocation period. New York requires SR-22 or FR-44 filing only for specific violations like DUI or driving without insurance, not for point-triggered suspensions, but reinstatement after a points suspension still requires a $100 suspension termination fee paid to the DMV and proof of future financial responsibility.

Once reinstated, you'll quote in the non-standard market with three active surcharges stacking simultaneously. Monthly premiums in this scenario often exceed $500/mo for minimum liability limits, and many non-standard carriers impose vehicle age restrictions or decline coverage for drivers under 25 with three events in three years.

How to Get Accurate Quotes With Both Events Disclosed

When shopping for coverage after adding a second event, disclose both the at-fault accident date and claim amount and the speeding ticket conviction date and speed charged. Carriers pull your MVR during underwriting, and any undisclosed event discovered after binding will void the quote and trigger a re-rate or policy cancellation. The re-rated premium will include both surcharges plus a potential misrepresentation penalty.

Request quotes from at least one preferred carrier, two standard carriers, and one non-standard carrier. Preferred carriers may decline, but some will quote if the accident was low-severity and the ticket was a minor speed. Standard carriers provide the most realistic comparison range for two-event records. Non-standard carriers serve as the fallback if standard carriers decline or quote above $300/mo.

Ask each carrier for the surcharge expiration timeline in writing. Some agents provide a year-by-year rate projection showing when each surcharge drops off and what your premium will be at each renewal assuming no new events. This projection helps you evaluate whether to stay with your current carrier or switch to a lower-cost option willing to write your record at a lower base rate.

What Coverage Level Makes Sense With Two Active Surcharges

Dropping from 100/300/100 liability limits to New York's 25/50/10 minimums saves $40-80/mo in base premium, but the percentage savings shrinks once surcharges apply. If your pre-surcharge premium was $150/mo for full limits and $90/mo for minimums, the post-surcharge premium might be $260/mo vs $210/mo—a smaller gap that may not justify the reduced protection.

Collision and comprehensive coverage on older vehicles becomes harder to justify when premiums exceed 10% of the vehicle's actual cash value annually. A car worth $6,000 with a $500 collision deductible and $180/year in collision premium made sense before the surcharges. At $320/year post-surcharge, you're paying 5.3% of the vehicle's value annually, and a single claim will total the car, leaving you with $5,500 after the deductible. Many two-event drivers drop collision on vehicles worth under $8,000 and bank the monthly savings.

Uninsured motorist coverage remains critical in New York, where 5-7% of drivers carry no insurance despite the state's mandatory coverage law. UM coverage costs $8-15/mo on most policies and protects you if the other driver flees or carries insufficient limits. Dropping UM to save $10/mo exposes you to unrecoverable medical bills and lost wages if you're hit by an uninsured driver.

When the Combined Surcharge Finally Drops and What Your Rate Does Next

Your premium will decrease in two stages as each surcharge expires. If your accident surcharge drops first, expect a 15-25% reduction at that renewal. When the ticket surcharge expires 6-12 months later, expect another 10-20% reduction. A driver paying $280/mo with both surcharges active might drop to $235/mo after the accident surcharge expires, then to $180/mo once the ticket surcharge rolls off.

Carriers won't automatically notify you when a surcharge expires. The rate decrease appears at renewal, but only if the carrier's underwriting system correctly applies the expiration date from their internal database. If your premium doesn't drop at the expected renewal, request a policy review and ask the carrier to confirm the surcharge expiration dates on file. Errors happen—especially when conviction dates or claim closure dates were entered incorrectly during a prior policy term.

Once both surcharges expire and your record is clean for 36 months from the most recent event, you can re-quote with preferred carriers that previously declined you. Many drivers see 30-50% savings by switching from a standard or non-standard carrier back to a preferred carrier after the surcharges clear, even if the preferred carrier quotes slightly higher than the standard carrier that carried them through the high-risk period.