An at-fault accident with bodily injury triggers both DMV points and a steep carrier surcharge that lasts longer than the points themselves. Here's the timeline, the rate impact, and what to expect at renewal.

The Double Hit: Points From Citation Plus Claim Surcharge

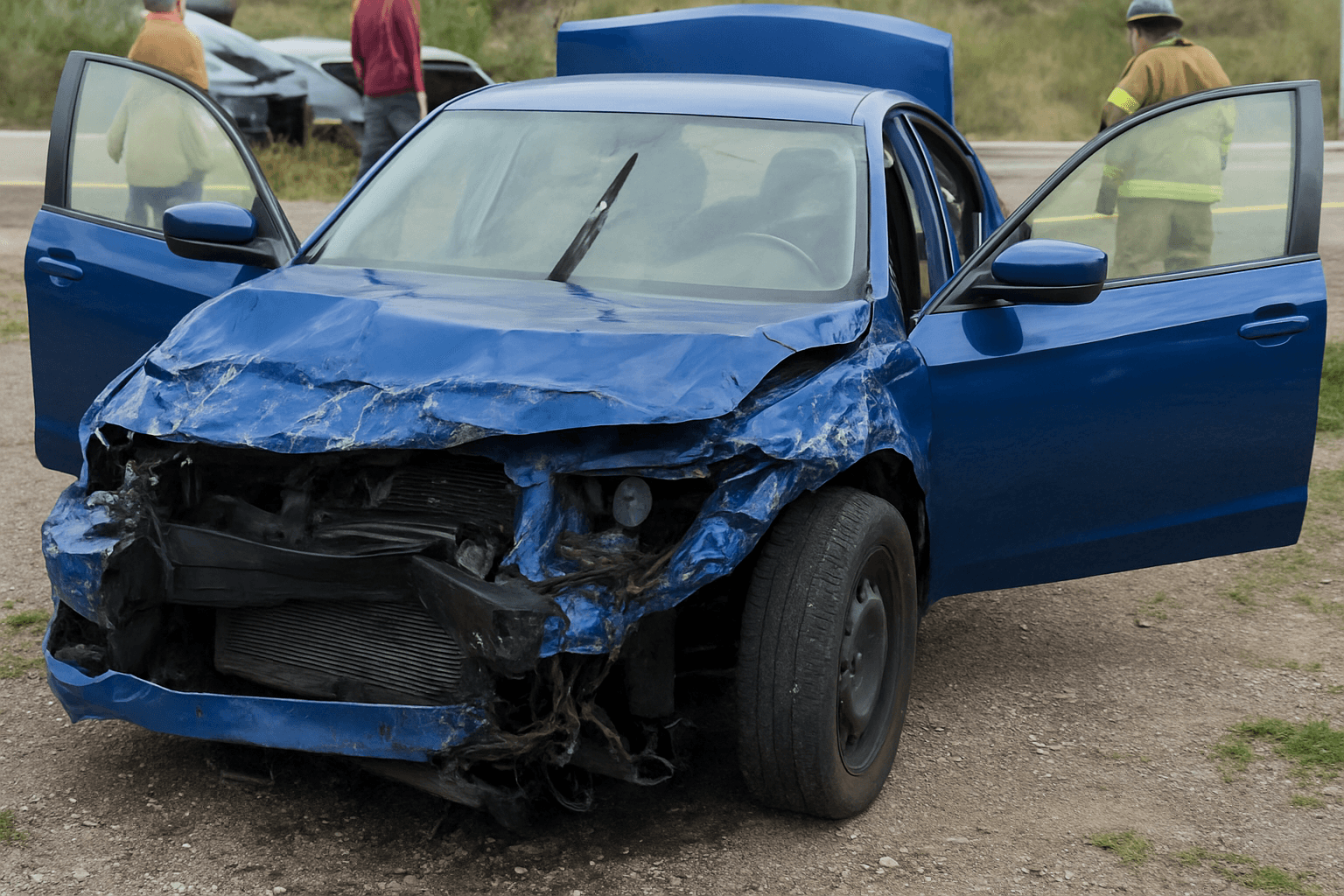

An at-fault accident with bodily injury triggers two separate insurance penalties. The first is the DMV points from the citation that caused the accident — typically careless driving, failure to yield, or following too closely. Those violations carry 2-4 points in most states and stay on your driving record for 3 years. The second is the bodily injury claim itself, which carriers surcharge independently of the points violation. That claim surcharge typically lasts 3-5 years and applies even if you weren't cited at the scene.

The points violation increases your rate 15-30% at most carriers. The bodily injury claim adds another 30-50% on top of that base increase, creating a stacked surcharge that can push your premium 60-90% higher at renewal. Preferred carriers like State Farm and GEICO will still renew you after a single bodily injury accident, but they apply both surcharges simultaneously. You pay the points penalty and the claim penalty as separate line items on the same policy.

This stacked structure explains why your rate doesn't drop significantly when your DMV points clear at the 3-year mark. The points surcharge ends, but the claim surcharge continues for another 1-2 years depending on your carrier's lookback period. Progressive and Allstate typically maintain bodily injury claim surcharges for 5 years from the accident date. Geico uses a 3-year window. The points window and the claim window run on separate clocks.

What Counts as Bodily Injury in Carrier Underwriting

Bodily injury means another person required medical treatment after the accident you caused. A trip to the emergency room counts. A chiropractor visit counts. An ambulance ride counts even if the person refused further treatment at the hospital. Carriers don't distinguish between a $2,000 injury claim and a $50,000 injury claim when setting your surcharge — both trigger the same percentage increase because both confirm you caused an accident severe enough to injure someone.

Property damage alone does not trigger the bodily injury surcharge. If you rear-ended someone and their car required $8,000 in repairs but neither occupant sought medical care, you'll pay the points surcharge from the citation but not the additional bodily injury penalty. The claim gets coded as property damage only, which most carriers surcharge at 20-35% rather than 40-60%. Your renewal notice will show the claim details and the specific surcharge applied.

Some carriers waive the bodily injury surcharge if the payout was under $1,000 and you've been with them more than 3 years. Erie and Auto-Owners occasionally apply this threshold. State Farm and Progressive do not — any bodily injury claim triggers the full surcharge regardless of payout amount or tenure. If your carrier's first notice of loss showed bodily injury, expect the surcharge even if the claimant's final medical bills were minimal.

Compare rates from carriers that work with drivers who have points

Standard carriers surcharge heavily after violations. These specialists price your specific record differently.

Get Your Free Quote✓ Violation Specialists✓ No Obligation✓ Licensed Carriers✓ All Point Levels

How Long Each Surcharge Lasts and When Rates Drop

The points surcharge ends when the points clear your DMV record, typically 3 years from the conviction date. If you were cited for careless driving on March 15, 2022, those points drop off your record on March 15, 2025, and your carrier removes the points surcharge at your next renewal after that date. You'll see a 15-25% rate decrease when the points penalty ends, but your premium will still be higher than your pre-accident rate because the bodily injury claim surcharge remains active.

The claim surcharge lasts 3-5 years from the accident date, not the conviction date. If the accident occurred on February 10, 2022, and you were cited 3 weeks later, the claim surcharge runs from February 10, 2022, through February 10, 2025 (3-year carrier) or February 10, 2027 (5-year carrier). Geico, USAA, and Travelers use a 3-year claim window. Progressive, Allstate, and Nationwide use 5 years. Liberty Mutual uses 5 years for bodily injury claims and 3 years for property damage only.

Your rate drops in stages. At the 3-year mark from conviction, the points surcharge ends and your rate drops 15-25%. At the 3-year or 5-year mark from the accident date, the claim surcharge ends and your rate drops another 30-40%. A driver paying $210/month after the accident might drop to $160/month when points clear, then to $120/month when the claim surcharge ends. You return to clean-record pricing only after both windows close and you've completed at least one full renewal cycle at the lower rate.

Preferred vs Standard Market After Bodily Injury

Most preferred carriers will renew you after a single at-fault bodily injury accident, but they reclassify you internally and raise your rate to the top tier of their preferred book. State Farm, Geico, and Progressive all maintain separate rate tiers within their preferred market — you move from tier 1 (clean record) to tier 4 or 5 (one major violation) but stay within the preferred underwriting structure. You're not dropped, but you're no longer eligible for good driver discounts or accident forgiveness unless you had already qualified before the accident.

A second bodily injury accident within 3 years usually triggers non-renewal at preferred carriers. Geico will send a non-renewal notice 60 days before your policy expires. State Farm typically allows one renewal after the second accident, then non-renews at the following term. You'll need to move to a standard-market carrier like Dairyland, National General, or The General. Standard market premiums for a driver with two bodily injury accidents in 3 years run $185-$310/month for state minimum liability, compared to $140-$210/month at a preferred carrier's highest tier.

Some drivers shop carriers immediately after the accident hoping to escape the surcharge. This rarely works. The accident appears on your CLUE report within 30 days of the claim, and every carrier you quote with pulls that report during underwriting. A new carrier will apply the same bodily injury surcharge as your current carrier, and you'll lose any tenure-based discounts you had built up. Shopping makes sense only if your current carrier non-renews you or if you're moving from preferred to standard market and need to compare non-standard options.

Coverage Decisions When Your Rate Doubles

Dropping to state minimum liability after a bodily injury accident is a common impulse when your premium jumps 70%. You caused an accident that injured someone once — the statistical likelihood you'll do it again within the next 3 years is higher than a clean-record driver, not lower. Minimum liability in most states covers $25,000 per person for bodily injury. If you cause a second accident and seriously injure someone, you're personally liable for medical bills, lost wages, and pain and suffering above that $25,000 cap.

Carrying $100,000/$300,000 liability limits costs an additional $15-$35/month over state minimums at most carriers, even with the bodily injury surcharge applied. That extra $25/month buys $75,000 more coverage per person and protects your savings, home equity, and wages from a judgment. Drivers with a recent bodily injury claim are exactly the population who should not reduce liability coverage, because they've demonstrated real-world collision risk and their premiums already reflect that elevated risk.

Collision and comprehensive coverage decisions depend on your vehicle's value. If you're driving a 2015 sedan worth $6,000 and your collision premium is $90/month with a $1,000 deductible, you're paying $1,080/year to insure a $6,000 asset. Drop collision, keep comprehensive for glass and theft at $18-$25/month, and bank the $65/month savings. If you're driving a 2021 vehicle worth $28,000 with $8,000 remaining on the loan, your lender requires collision and comprehensive until the loan is paid. You can raise your deductible from $500 to $1,000 and cut $20-$40/month from your premium without dropping required coverage.

Does a Defensive Driving Course Reduce the Surcharge?

Completing a state-approved defensive driving course can remove points from your DMV record in 32 states, but it does not remove the bodily injury claim from your insurance record. The course addresses the citation — careless driving, failure to yield, or whatever violation caused the accident. If your state allows point reduction through defensive driving and you complete the course within 90 days of conviction, the points drop off your DMV record immediately and your carrier removes the points surcharge at the next renewal.

The bodily injury claim itself stays on your CLUE report for 7 years regardless of defensive driving course completion. Your carrier will continue applying the claim surcharge for the full 3-year or 5-year period even if you removed the points. The two penalties run on separate tracks — the points reflect the traffic violation, the claim reflects the insurance payout. Removing one does not affect the other.

Some carriers offer a claim forgiveness program that waives the first at-fault accident surcharge if you've been claim-free for 5 years prior. State Farm, Allstate, and Nationwide offer this as an optional endorsement you must purchase before the accident occurs. If you already had accident forgiveness active on your policy when the bodily injury accident happened, your carrier waives both the points surcharge and the claim surcharge and your rate stays flat at renewal. You cannot buy accident forgiveness after the accident — it must be in force at the time of loss. After your carrier forgives one accident, the endorsement resets and you must remain claim-free for another 5 years to re-qualify.

When Points Trigger License Suspension on Top of Surcharges

An at-fault bodily injury accident that adds 3-4 points can push you over your state's suspension threshold if you already had points from prior violations. Most states suspend licenses at 12 points in 12 months or 18 points in 24 months. If you entered the accident year with 9 points from two prior speeding tickets, and the careless driving citation from the bodily injury accident adds 4 points, you hit 13 points and trigger an automatic suspension.

Once your license is suspended, your carrier will non-renew your policy at the next renewal date. You cannot legally drive during the suspension period, and most carriers will not reinstate coverage until your license is fully reinstated and you've filed SR-22 if your state requires it. Reinstatement after a points suspension typically requires paying a $200-$500 reinstatement fee, completing a driver improvement course, and filing SR-22 for 3 years. Your premium after reinstatement will reflect the bodily injury surcharge, the SR-22 filing fee ($25-$50/year), and a lapse surcharge if any gap in coverage occurred during suspension.

SR-22 filing alone does not increase your rate — it's a compliance certificate your carrier files with the DMV confirming you carry the state-required liability minimums. But needing SR-22 usually means you're shopping in the non-standard market because preferred carriers rarely write policies for drivers with suspended licenses, and non-standard market base rates are 40-80% higher than preferred carriers before any violation surcharges apply. Expect premiums of $215-$380/month for state minimum liability with SR-22 after a points suspension combined with a bodily injury claim.